Table of contents

The rapidly expanding world of EU e-commerce comes with layers of regulatory requirements, particularly when it comes to Value-Added Tax (VAT). Navigating multiple national VAT registrations can be a daunting hurdle for online retailers, leading to administrative headaches and compliance risks. Discover how a single VAT number can transform the way businesses operate, streamline cross-border sales, and open doors to new markets while keeping compliance simple and efficient.

vat compliance made easy

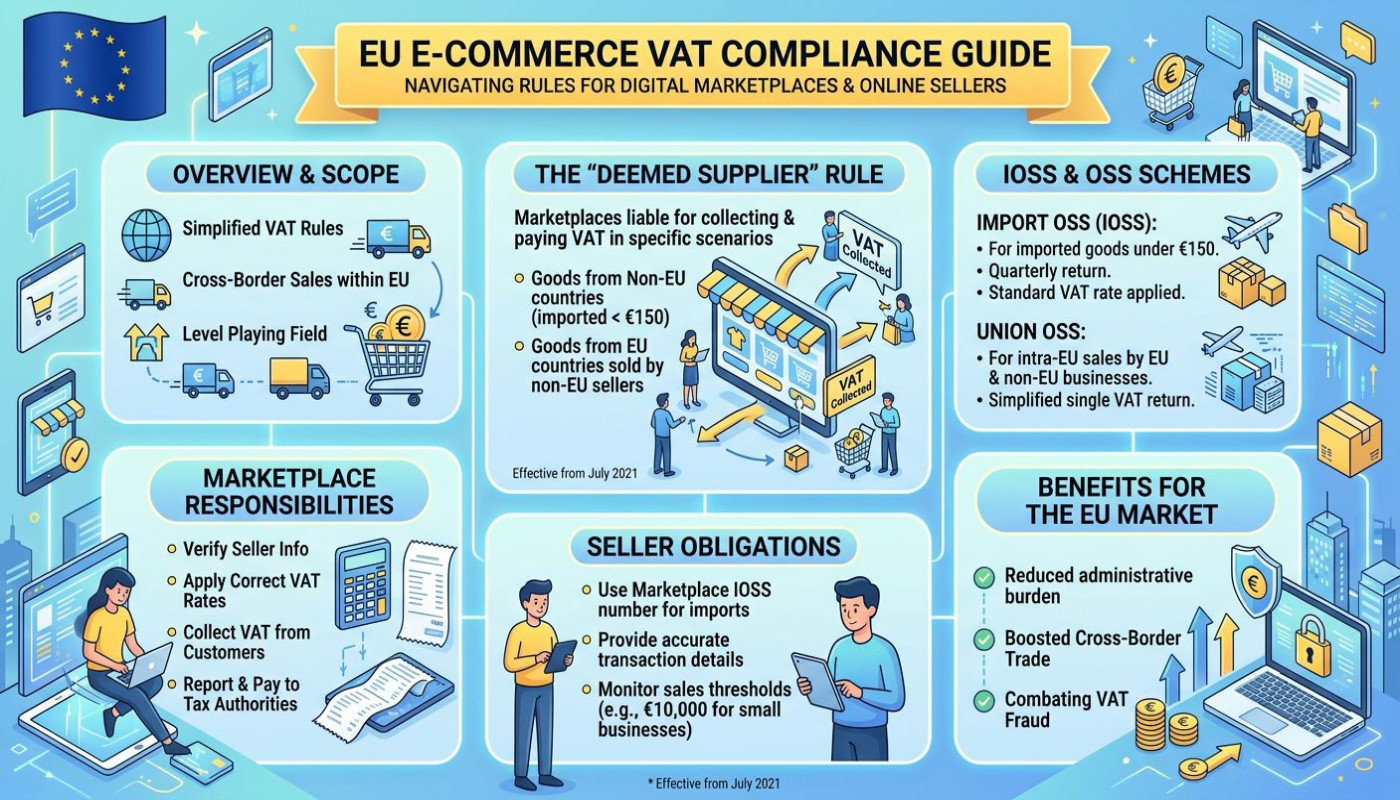

The One-Stop Shop (OSS) scheme revolutionizes the way online retailers handle VAT obligations within the European Union. By using the OSS VAT system, businesses engaging in cross-border sales can now register for VAT in a single EU member state instead of needing multiple EU VAT registrations in each country where customers are located. This streamlined approach supports e-commerce compliance by enabling businesses to declare and pay VAT due across all relevant EU countries through one quarterly return, managed via a single online portal. The OSS mechanism directly addresses the complexities and administrative burdens that used to hamper growth and expansion for online retailers, especially those catering to consumers in several EU states.

Previously, companies had to grapple with the intricacies of local tax registrations, reporting, and payment procedures that varied widely between member states. The implementation of the OSS VAT system removes these barriers, offering a centralized solution that is both time-saving and cost-effective. This is especially beneficial for SMEs and growing businesses looking to scale their operations without being bogged down by fragmented VAT compliance requirements. For senior EU tax consultants, the technical term One-Stop Shop (OSS) represents a pivotal harmonization tool that efficiently aggregates all VAT reporting for EU-wide B2C sales under a single national jurisdiction, reducing compliance risks and errors linked to inconsistent tax processes.

Moreover, the OSS VAT system aligns with modern e-commerce trends, where online retailers increasingly operate in multiple markets simultaneously. It supports efficient cross-border sales management while facilitating accurate, consolidated VAT reporting and payment. Businesses can further explore simplified EU VAT procedures for distance sales, including topics such as IOSS registration, by visiting resources like IOSS registration for detailed guidance on registration and returns. This integrated approach reflects the EU’s commitment to making e-commerce compliance as straightforward as possible for all market participants.

reducing administrative burden

Utilizing a single VAT number across the European Union streamlines compliance for businesses engaged in multi-country sales. This approach dramatically reduces paperwork by eliminating the necessity of registering for separate VAT numbers in each EU member state. Instead, businesses can centralize their EU tax reporting, managing all required documentation under one identification number. Such administrative efficiency not only cuts down on the time and resources spent on complex tax procedures but also minimizes the risk of errors or inconsistencies in filings. VAT simplification through this unified system allows companies to submit one VAT return, a comprehensive report detailing all taxable transactions, rather than completing multiple, country-specific reports. This process ensures seamless movement of goods and smooth transactions across borders, making the management of tax obligations far more straightforward for businesses operating throughout the EU. Content provided by a leading VAT compliance specialist.

expanding market access

Obtaining one VAT number allows businesses to fully leverage the EU single market by eliminating the complexities typically associated with VAT registration in each member state. This single identifier streamlines cross-border commerce, making it much easier for companies to sell their goods and services digitally across the entire European Union. With only one VAT registration, businesses can efficiently manage tax obligations regardless of where customers are located, thereby supporting rapid market expansion and unlocking new growth opportunities. The technical concept of intra-community supply refers to goods sold and shipped between different EU countries, which are generally VAT-exempt at the point of sale, provided both buyer and seller are VAT-registered. This mechanism significantly lowers barriers and administrative burdens, resulting in smoother, more cost-effective operations for digital sales and enabling even smaller enterprises to compete in multiple markets. The information presented is composed by an expert in EU e-commerce regulations, ensuring reliable guidance on maximizing the benefits of the single VAT number system.

enhancing legal certainty

Using a single VAT number across multiple EU countries offers significant legal certainty for online businesses, especially under the evolving landscape of EU tax law. When a business operates with one VAT number, the risk of non-compliance decreases because transactions are reported uniformly, minimizing discrepancies that often trigger VAT audits. This harmonized approach reduces compliance risk by ensuring that all sales, returns, and tax obligations are consistently tracked and reported to the relevant authorities. In cross-border transactions, a fiscal representative—an entity appointed in certain EU countries to handle VAT obligations for businesses without local establishments—can facilitate smoother interactions with tax offices, helping to safeguard against administrative errors. A single VAT number streamlines communication, making outcomes in VAT audits more predictable and ensuring businesses can operate with confidence within the framework of EU tax law.

streamlining digital platforms

A unified VAT number dramatically enhances the efficiency of operating within the digital marketplace, particularly for intermediary platforms that connect multiple sellers and buyers. VAT simplification under the One-Stop Shop scheme aligns with EU VAT rules, allowing digital platforms to manage tax obligations centrally rather than across multiple jurisdictions. This makes onboarding new sellers smoother, as platforms can ensure platform compliance without requiring each seller to navigate the complexities of local legislation. With e-commerce integration becoming increasingly advanced, such a streamlined process reduces administrative burdens, enabling both sellers and the platform to focus on growth and innovation. For an intermediary platform, which facilitates transactions on behalf of third-party sellers, this setup minimizes risk and ensures accurate VAT collection and remittance, making cross-border trade more accessible and efficient across the European Union.

Similar articles